Selling an accountancy practice is one of the most significant decisions an accountant can make. After years of building client relationships, developing a reputation, and growing recurring revenue, reaching an agreement with a buyer can feel like crossing the finish line.

However, agreeing on a sale price is not the end of the journey.

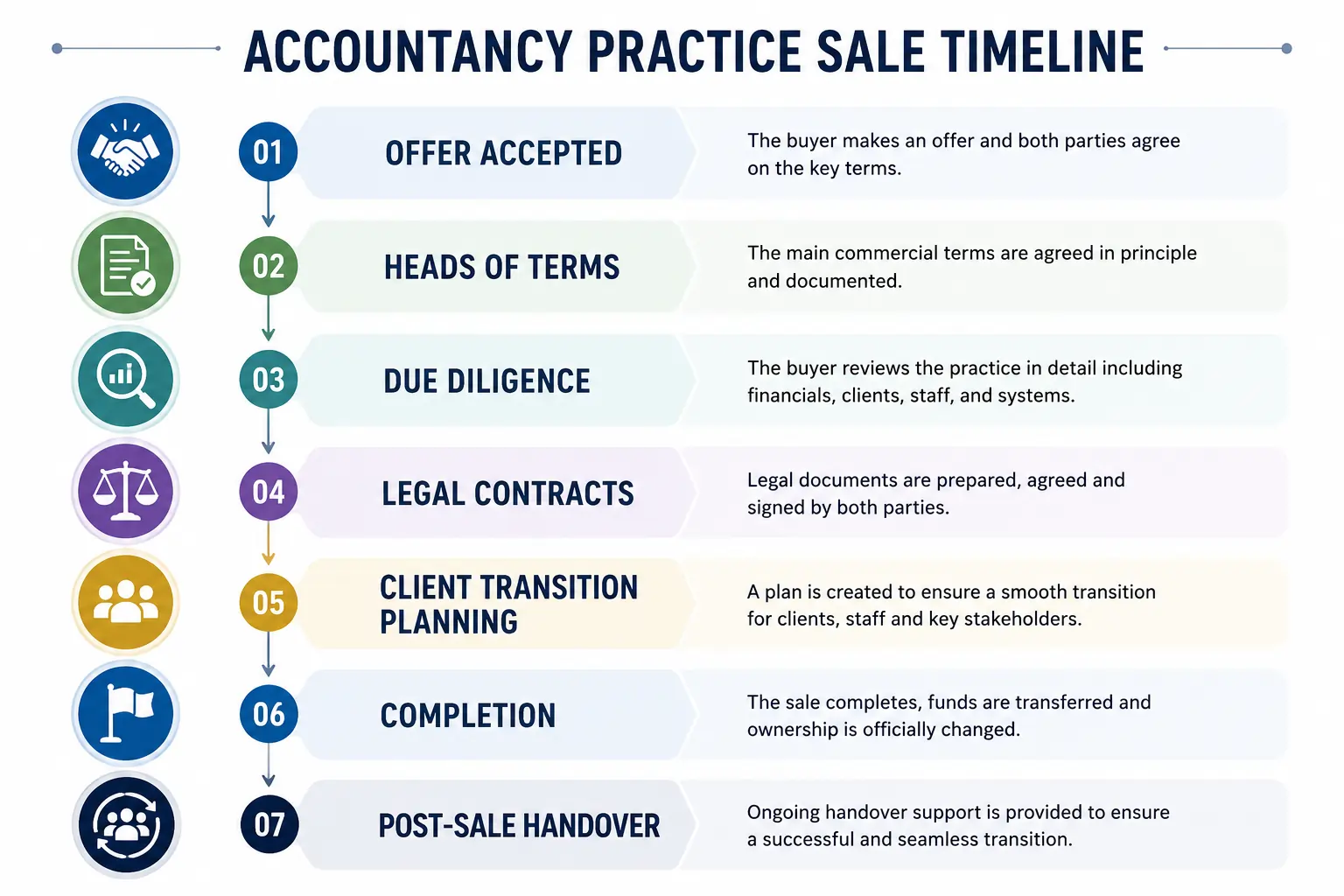

In reality, the period between accepting an offer and completing the sale is often the most important stage of the entire transaction. This is where due diligence takes place, legal agreements are negotiated, client transition plans are developed, and both parties work together to ensure a smooth transfer of ownership.

Many sellers underestimate the amount of work required after an agreement is reached. Delays, compliance concerns, confidentiality issues, and client retention challenges can all affect the outcome of the sale if not managed properly.

This guide explains exactly what happens after you agree to sell your accountancy practice and how to navigate each stage successfully.

Key Takeaways

- Accepting an offer is only the beginning of the sale process.

- Heads of Terms establish the framework for the transaction.

- Buyers conduct detailed due diligence before committing fully.

- Client confidentiality must be protected throughout the process.

- Legal agreements safeguard both buyer and seller.

- Client transition planning plays a major role in deal success.

- Completion may take several weeks or months after the initial agreement.

- Proper preparation helps avoid delays and protects practice value.

The Problem: Many Sellers Think the Hard Part Is Over

Finding the right buyer and agreeing on a price often takes months of preparation and negotiation.

As a result, many accountants assume the most difficult stage is behind them.

The reality is different.

Most transactions encounter challenges after the offer has been accepted. Buyers want reassurance that the information provided is accurate. Legal advisors review contracts carefully. Clients need to be transitioned smoothly. Regulatory obligations must be satisfied.

Without proper planning, these stages can delay completion or even jeopardize the deal entirely.

The good news is that understanding the process in advance allows sellers to prepare effectively and avoid unnecessary complications.

Step 1: Heads of Terms (HoT)

After a buyer and seller reach an agreement in principle, the next step is usually the preparation of Heads of Terms.

Heads of Terms are generally non-binding but serve as a roadmap for the transaction.

They outline the key commercial points agreed between both parties before legal work begins.

Typical areas covered include:

- Agreed sale price

- Payment structure

- Earn-out arrangements

- Completion timetable

- Exclusivity period

- Confidentiality obligations

- Post-sale involvement

Although not legally binding in most cases, Heads of Terms help reduce misunderstandings later in the process.

Heads of Terms Checklist

| Usually Included | Purpose |

|---|---|

| Sale Price | Agreed transaction value |

| Payment Terms | How and when payments are made |

| Earn-Out Structure | Future performance payments |

| Completion Date | Proposed sale timeline |

| Exclusivity Period | Protects buyer negotiations |

| Confidentiality Requirements | Protects sensitive information |

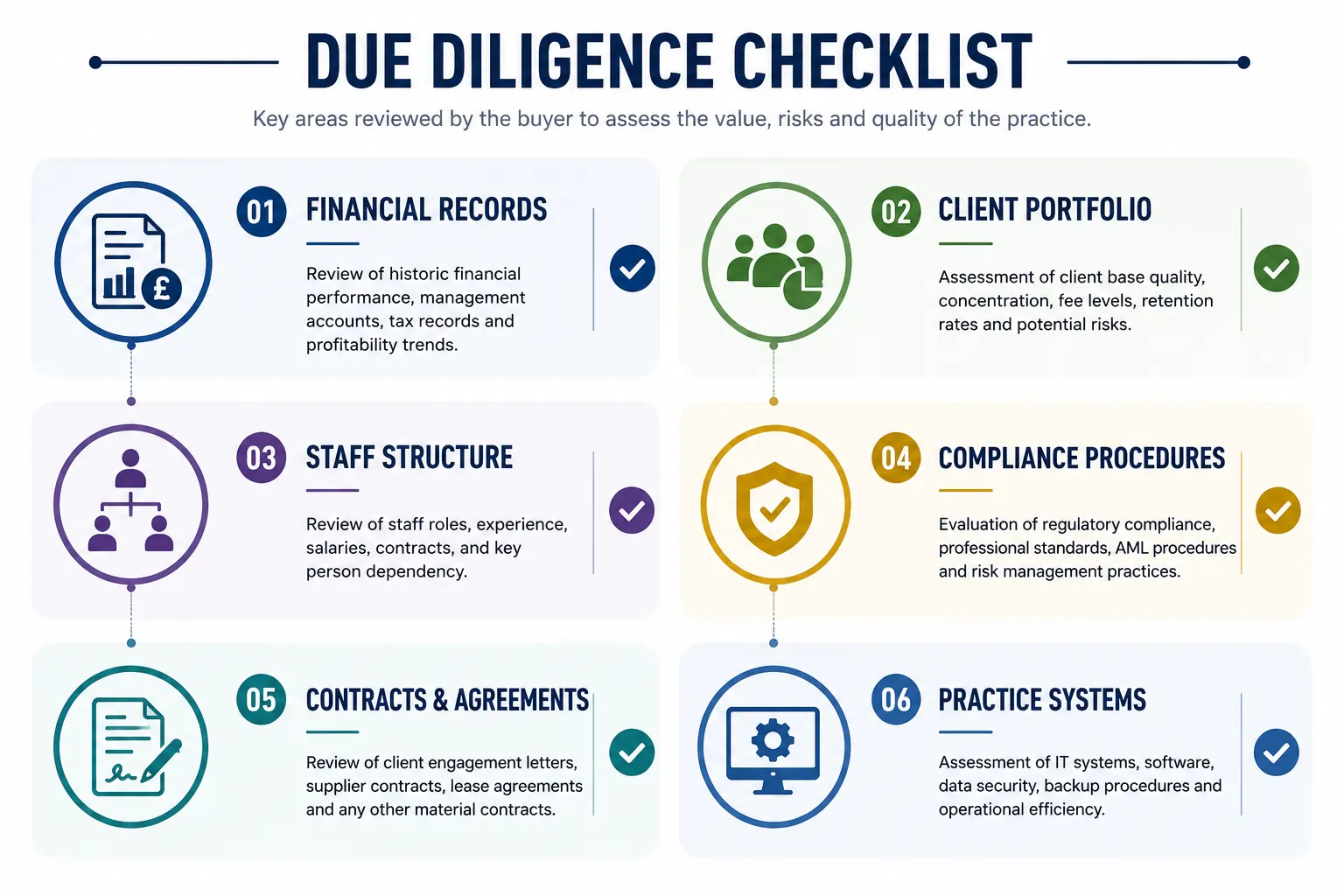

Step 2: Buyer Due Diligence

Due diligence is often the most detailed stage of the transaction.

The buyer will review the practice thoroughly to confirm that the business matches the information provided during negotiations.

This stage protects the buyer from unexpected risks and ensures the valuation remains justified.

Financial Due Diligence

The buyer will typically examine:

- Revenue history

- Recurring fee income

- Profitability trends

- Work in progress

- Debtor balances

- Client concentration

Strong financial records help build confidence and speed up the process.

Client Portfolio Review

Client relationships are often the most valuable asset in an accountancy practice.

The buyer may review:

- Client retention rates

- Service mix

- Average fees

- Key client dependencies

- Contract arrangements

The objective is to assess the stability and sustainability of future revenue.

Operational Review

The buyer will also evaluate how the practice operates.

Areas commonly reviewed include:

- Staff structure

- Practice management systems

- Software platforms

- Internal procedures

- Workflow processes

Efficient operations increase the attractiveness of the practice.

Compliance Review

Compliance is particularly important within the accountancy sector.

Buyers may review:

- Anti-Money Laundering (AML) procedures

- GDPR compliance

- Professional standards

- Regulatory records

- Risk management policies

Any weaknesses discovered during due diligence may influence the final transaction terms.

Step 3: Protecting Client Confidentiality

One of the most sensitive issues during a practice sale is client confidentiality.

Accountants have a professional obligation to protect client information.

Buyers need enough information to assess the business, but sensitive data must be handled appropriately.

This balance is usually achieved through:

- Non-Disclosure Agreements (NDAs)

- Controlled information sharing

- Anonymized client lists

- Secure document storage

Initially, client information is often presented anonymously. More detailed information may be disclosed later under strict confidentiality arrangements.

Maintaining client trust throughout the process is essential.

Step 4: Negotiating the Sale Agreement

Once due diligence progresses successfully, legal advisors begin preparing the formal sale documentation.

The main legal document is usually the Sale and Purchase Agreement (SPA).

This agreement sets out the legal obligations of both parties.

Key Legal Documents

| Document | Purpose |

|---|---|

| Sale and Purchase Agreement | Main transaction contract |

| NDA | Protects confidential information |

| Warranty Schedule | Seller disclosures |

| Restrictive Covenants | Protect buyer’s investment |

| Transition Agreement | Defines post-sale support |

Common Legal Clauses

The SPA may include:

- Payment terms

- Completion conditions

- Warranties

- Indemnities

- Non-compete provisions

- Handover obligations

Professional legal advice is highly recommended to ensure your interests are protected.

Step 5: Staff Communication

Employees often play a crucial role in maintaining client relationships and ensuring business continuity.

For this reason, communication regarding the sale should be handled carefully.

Premature disclosure may create uncertainty, while delayed communication can affect trust and morale.

The timing of staff announcements should be coordinated with legal advisors and the buyer.

When handled effectively, transparent communication helps:

- Maintain staff confidence

- Reduce turnover risks

- Support client retention

- Ensure operational stability

Staff engagement often contributes significantly to a successful transition.

Step 6: Client Transition Planning

Client retention is one of the most important factors influencing the success of an accountancy practice sale.

The buyer is not simply purchasing a client list. They are acquiring ongoing relationships and recurring revenue.

A structured transition plan helps maintain confidence and continuity.

Effective Client Transition Strategies

Introduce the Buyer Personally

Clients are more likely to remain with the practice when introduced directly by the seller.

Explain the Benefits

Clients should understand how the acquisition benefits them.

Maintain Service Continuity

Avoid disruptions to service delivery during the transition period.

Focus on Key Clients

Priority should be given to high-value relationships.

Step 7: Completion Day

Completion marks the official transfer of ownership.

On this day:

- Contracts are signed

- Funds are transferred

- Ownership changes hands

- Agreed obligations become effective

Although completion is a significant milestone, it is often followed by a transition period.

Completion Checklist

| Task | Complete |

|---|---|

| Contracts Signed | ✓ |

| Funds Received | ✓ |

| Client Records Transferred | ✓ |

| Staff Communication Completed | ✓ |

| Compliance Requirements Met | ✓ |

Step 8: Post-Sale Support Period

Many practice sales include a post-sale support arrangement.

The seller may remain involved temporarily to help ensure a smooth transition.

This support can include:

- Client introductions

- Staff mentoring

- Process explanations

- Relationship management

- Technical assistance

The duration varies depending on the transaction structure.

The Problem: Sellers Focus on Price Instead of Transition

Many accountants concentrate heavily on achieving the highest possible valuation.

While price is important, the success of a practice sale depends on more than the agreed figure.

Factors such as:

- Client retention

- Staff stability

- Smooth handover

- Effective communication

often have a greater influence on long-term success.

Poor transition planning can damage the value of the deal for both parties.

The Solution: Plan for Completion Before Signing

The most successful practice sales begin preparing for completion long before contracts are signed.

Preparation should include:

- Organizing financial records

- Reviewing compliance procedures

- Planning client communications

- Preparing staff engagement strategies

- Establishing transition support arrangements

A proactive approach reduces delays and improves outcomes.

Common Mistakes Sellers Make

Incomplete Documentation

Missing records often delay due diligence.

Weak Client Communication

Poor communication can increase client attrition.

Underestimating Transition Time

Many sellers assume handovers happen quickly.

Ignoring Staff Concerns

Staff uncertainty may affect retention.

Delaying Preparation

Waiting until after accepting an offer often creates avoidable challenges.

Common Seller Mistakes

| Mistake | Consequence |

|---|---|

| Incomplete Records | Transaction Delays |

| Poor Client Communication | Client Loss |

| Weak Transition Planning | Reduced Retention |

| Lack of Preparation | Increased Stress |

| Compliance Gaps | Legal Risks |

Conclusion

Agreeing to sell your accountancy practice is a major achievement, but it is only the beginning of the transaction process.

The period between accepting an offer and completing the sale involves careful planning, detailed due diligence, legal documentation, client transition management, and post-sale support.

Understanding each stage allows sellers to prepare effectively, reduce risks, and maximize the likelihood of a successful outcome.

The most successful practice sales are not simply about securing the best price. They are about creating a smooth transition that protects clients, supports staff, and preserves the value of the business for both buyer and seller.

By approaching the process strategically and seeking professional advice where needed, accountants can move through the sale confidently and achieve a successful result.