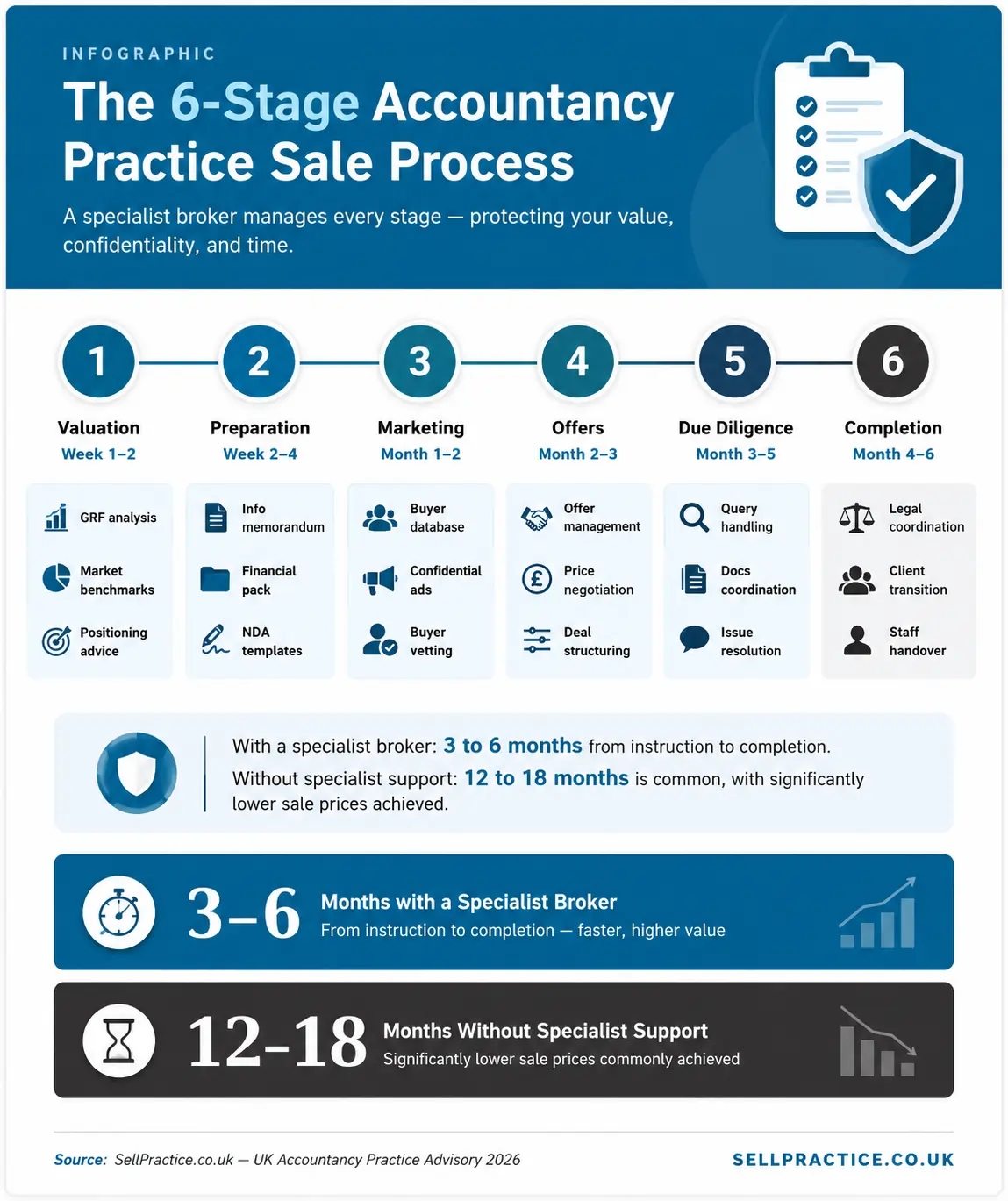

What Is a Specialist Accountancy Practice Broker?

Before examining the benefits in detail, it is worth being precise about what distinguishes a specialist accountancy practice broker from a general business broker or a DIY sale approach.

A specialist broker operates exclusively or primarily in the accountancy practice market. They understand how practices are valued, who the active buyers are, what buyers look for, and how deals in this sector are typically structured.

They work with this market every day, which means their market intelligence is current, their buyer relationships are live, and their knowledge of what constitutes a good deal is grounded in real transaction data rather than general business sale principles.

This distinction matters enormously. An accountancy practice is not a generic business. Its value is calculated primarily on gross recurring fees (GRF) using multiples that vary depending on the practice type, client quality, technology stack, geographic location, and owner dependence. A general business broker who typically sells retail businesses or manufacturing companies will not understand these nuances, will likely undervalue the practice, and will not have access to the pool of qualified buyers who are actively seeking accountancy acquisitions in 2026.

What specialist mean in practice

A specialist accountancy broker will have sold dozens or hundreds of practices, will maintain a database of qualified buyers who have already been credit-checked and assessed for cultural fit, will know current GRF multiples by practice type and region, and will have handled the specific legal and structural issues that arise in accountancy practice transactions.

KEY TAKEAWAYS

- A specialist broker has a pre-qualified buyer database – dramatically reducing time to find the right match.

- Accurate GRF-based valuation prevents underselling – the single most costly mistake in practice sales.

- Managed confidentiality protects staff, clients, and referral relationships throughout the process.

- Expert deal structuring on earn-outs, clawbacks, and payment terms can add tens of thousands to net proceeds.

- Specialist brokers typically achieve sale completion in 3 to 6 months vs 12 to 18 months unassisted.

- The fee a specialist broker charges is almost always recovered through a higher achieved sale price.\

Accurate Valuation – Avoiding the Most Costly Mistake

The single most expensive mistake an accountancy practice owner can make is not understanding the true value of their practice before entering the market. Underselling by even 0.1x GRF on a practice with £500,000 in gross recurring fees costs £50,000.

On a £1 million GRF practice, that same misjudgement costs £100,000. These are not hypothetical numbers – they represent the routine difference between what sellers achieve with and without specialist guidance.

How specialist brokers value accountancy practices

The primary valuation methodology for accountancy practices in the UK is based on gross recurring fees, with multiples typically ranging from 0.8x to 2.0x GRF depending on a range of factors.

A specialist broker understands all of these factors and how they interact. Practices with high recurring revenue – where clients are on standing direct debits or monthly billing arrangements – attract premium multiples because buyers are acquiring a predictable, stable income stream.

Practices where fees are predominantly ad hoc, seasonal, or based on one-off work command lower multiples because the future revenue is less certain.

The technology profile of a practice has become increasingly significant to valuation in recent years. Cloud-based practices – those operating on Xero, QuickBooks, or similar platforms with full digital workflows – attract meaningfully higher interest from buyers, particularly from the private equity-backed consolidators who are now a significant force in the UK accountancy acquisition market.

These buyers are paying a premium for practices that can be integrated quickly and at low cost into their existing infrastructure.

A practice still operating on desktop software and paper files is not only harder to integrate – it signals a client base that may be more resistant to change, which represents acquisition risk.

Owner dependence – the valuation killer most sellers underestimate

Perhaps the most commonly overlooked factor in practice valuation is owner dependence. If the practice’s client relationships are primarily personal to the owner – if clients would be likely to follow the owner out of the door rather than transfer to a new owner – then a buyer is essentially paying for goodwill that may not transfer.

Specialist brokers identify this issue early and work with sellers to address it before going to market. This might involve introducing clients formally to other team members, ensuring client files are complete and accessible without the owner’s knowledge, or restructuring client service delivery so that relationships are with the firm rather than the individual.

Addressing owner dependence before sale is not just about honesty – it directly affects the multiple a buyer will pay and the terms they will offer.

A practice where the owner can walk away on day one and client retention is high commands a full GRF multiple at favourable payment terms.

A practice where client retention depends on a lengthy earn-out period and the ongoing involvement of the seller typically commands a lower effective multiple when the earn-out conditions are factored in.

Current market multiples (2026)

Sole practitioner: 0.8x to 1.2x GRF. Small partnership (2-4 staff): 1.0x to 1.4x GRF. Cloud-based or scalable practice: up to 1.8x GRF. Advisory-led practice: 1.5x to 2.0x or more GRF. PE-backed or larger firm acquisitions: 14x to 15x EBITDA. Source: Bains Watts, AccountantsForSale.co.uk, SellPractice 2026.

2. Access to Pre-Qualified Buyers – The Network Advantage

One of the most significant and least visible advantages of using a specialist broker is access to their buyer database. This is not simply a list of names – it is a curated, maintained, and regularly updated database of individuals and firms who have actively expressed interest in acquiring an accountancy practice, have been assessed for financial credibility, and have provided information about the type of practice they are looking for in terms of size, geography, service mix, and client profile.

When a seller instructs a specialist broker, the right buyers are typically identified within days, not months. The broker knows who is looking for a sole practitioner practice in the South East, who wants a cloud-based practice with a strong small business client base in the Midlands, and who is looking for a practice with significant tax advisory revenue. This matching capability compresses the timeline dramatically and immediately improves the quality of offers received, because the buyers who are introduced are genuinely interested and qualified to complete.

Why buyer quality matters as much as buyer quantity

A common misconception among sellers who pursue DIY routes is that getting more buyers to look at the practice is always better. In reality, the wrong buyers cause significant damage. An unqualified buyer who cannot secure financing wastes months of management time and creates confidentiality risk as information about the sale spreads. A buyer who is not a good cultural fit for the client base may make an offer, only for due diligence to reveal issues that cause the deal to collapse – at which point the practice has been on the market for six months, confidentiality may have been compromised, and the seller has to start again.

Specialist brokers filter relentlessly. They pre-screen buyers on financial capacity, acquisition experience, geographic focus, and cultural fit before making an introduction. They also manage the information flow – ensuring that sensitive financial information is only shared under a non-disclosure agreement with buyers who have genuinely progressed through an initial assessment stage. This discipline protects the seller throughout the process.

CASE STUDY: SURREY BOOKKEEPING AND ACCOUNTS PRACTICE

From 18 months stalled to sold in 4 months – the buyer database difference

Background: A sole practitioner with 120 clients and annual GRF of £180,000 had been attempting to sell her practice independently for 18 months. She had advertised on a general business sale platform and had received several enquiries, but none had progressed beyond an initial conversation.The problem: Without access to a specialist buyer database, she was reaching general business buyers who did not understand the sector, could not assess the quality of her client book, and were not positioned to make credible offers. Her asking price of 1.0x GRF was reasonable, but without the right buyers, the price was irrelevant.

What changed: She instructed SellPractice to manage the sale. Within three weeks, four qualified buyers had been identified from the existing database, all of whom were actively looking for a practice of this size in Surrey. Two submitted formal offers within six weeks.

Outcome: The practice sold at 1.15x GRF – 15 percent above her original asking price – to a small regional firm looking to expand its geographic footprint. Completion took four months from instruction. The buyer was introduced exclusively through the broker database and had never appeared on any public listing.

3. Confidentiality – Protecting What You Have Built

Confidentiality is not simply a nice-to-have in an accountancy practice sale – it is a fundamental requirement. Unlike most business sales, an accountancy practice sale carries specific and serious confidentiality risks that can destroy value if not managed carefully. Staff who learn of a potential sale may begin looking for other positions. Clients who discover their practice is for sale may pre-emptively move to another firm. Referral partners – solicitors, financial advisers, and mortgage brokers who regularly refer clients – may redirect those referrals if they are uncertain about the future of the practice. Any of these outcomes can reduce the value of the practice before a sale is even agreed.

How specialist brokers manage confidentiality

A specialist broker operates under a rigorous confidentiality protocol from the first day of instruction. The practice is never identified in any public marketing by name or by easily identifiable details. Marketing materials describe the practice in terms that will be recognisable to informed buyers without revealing the identity of the firm – for example, describing it as a cloud-based practice with 150 small business clients in the South East, without naming the firm, the town, or any identifiable clients.

Non-disclosure agreements are executed before any identifying information is shared with prospective buyers. These agreements are tailored to the accountancy sector and cover not just the financial information but also the identity of the practice, its client list, its staff, and its referral relationships. The broker manages the flow of information through staged disclosure – releasing more detail only as buyers progress through defined stages of the acquisition process and demonstrate serious intent.

Without this discipline, confidentiality failures in DIY sales are common. A seller who advertises their practice directly, even on a specialist platform, inevitably reveals enough identifying information for staff, clients, and competitors to identify the firm. The consequences can be severe: a senior member of staff who discovers the practice is for sale and decides to leave takes not just their salary but potentially a portion of the client relationships with them, reducing the very thing the buyer is paying for.

Staff communication strategy

Most specialist brokers advise a phased communication strategy with staff. Senior staff who are essential to the transition may be informed once heads of terms are agreed and kept engaged with appropriate retention incentives. Junior staff are typically informed at completion. The broker can advise on the precise timing based on the specific dynamics of each practice.

4. Deal Structuring – Where Real Money Is Made or Lost

The headline sale price is not the same as the money you receive. This is one of the most important financial insights in any accountancy practice sale, and it is the area where sellers who proceed without specialist advice most frequently lose significant value. The structure of a deal – how the total consideration is paid, over what period, subject to what conditions – can change the effective value of the same headline price by tens of thousands of pounds.

Earn-outs and why they need expert structuring

The majority of accountancy practice sales involve some form of deferred consideration or earn-out arrangement. A buyer is not simply purchasing a fixed asset – they are purchasing a client relationship book, and client retention after a change of ownership is never guaranteed. Buyers therefore typically want to pay part of the consideration upfront and retain the remainder, releasing it over one to three years based on actual client retention. This is a legitimate commercial structure, but the precise terms of an earn-out – the base level of retention required, what counts as retained revenue, how disputes are resolved, and what the seller can and cannot do during the earn-out period – have an enormous impact on whether the full headline price is actually received.

Specialist brokers have seen hundreds of earn-out structures and know which terms are reasonable, which are predatory, and which create unacceptable risk for the seller. They will negotiate the earn-out conditions on the seller’s behalf, push back on unreasonable clawback provisions, and ensure that the definition of retained revenue is clear and measurable. This alone frequently justifies the broker’s fee.

Payment terms, phasing, and tax implications

The tax treatment of a practice sale depends significantly on how the consideration is structured and paid. A lump sum payment triggers different tax consequences from staged payments spread over multiple years. Payments classified as salary or consultancy during a transition period are taxed as income rather than as capital gains. The availability of Business Asset Disposal Relief – previously Entrepreneurs’ Relief – on capital gains may apply to some elements of the consideration but not others, depending on how the deal is structured. A specialist broker will work alongside the seller’s tax adviser to ensure the deal structure is optimised not just for headline price but for net proceeds after tax.

CASE STUDY: LEEDS CHARTERED ACCOUNTANCY FIRM

How deal structuring added £65,000 to net proceeds on a £600,000 sale

Background: A chartered accountancy firm with GRF of £420,000 received an unsolicited offer of £600,000 from a regional consolidator. The seller was initially inclined to accept without broker involvement, believing the offer was fair.What a specialist review revealed: The offer was structured as £480,000 on completion and £120,000 deferred over two years, with a clawback provision that defined retained revenue as clients billing 100% of their prior year fee within the earn-out period. This condition was extremely difficult to meet in practice, as fee increases and scope changes would count against retention.

What the broker negotiated: The earn-out definition was changed to clients billing 85% or more of prior year fees. The deferred payment period was compressed from 24 months to 18 months. A personal goodwill element was restructured to attract Business Asset Disposal Relief rather than income tax treatment.

Outcome: Final net proceeds increased by approximately £65,000 against what the seller would have received under the original terms. The broker fee was covered more than three times over by the improved deal structure alone.

5. Speed to Completion – Time Is Not on Your Side

Time is a genuinely dangerous factor in accountancy practice sales. The longer a practice is on the market, the greater the risk that confidentiality is compromised, that key staff become unsettled, that clients pick up signals of uncertainty, and that buyers begin to wonder why the practice has not yet sold. A practice that has been advertised for twelve months without a completed sale raises questions in buyers’ minds, even if the reasons for the delay have nothing to do with the quality of the practice itself.

Specialist brokers consistently achieve faster completions than DIY sales or general broker-managed sales. This is a function of three factors: immediate access to a pre-qualified buyer pool, an efficient and structured process with defined stages and timelines, and experienced management of the deal through the stages that most commonly cause delays – due diligence, legal documentation, and regulatory considerations.

The regulatory dimension is often overlooked. ICAEW, ACCA, and other professional bodies have specific requirements around the transfer of practising certificates, the transfer of client files, and the notification of regulatory changes. A general business broker or a seller managing their own transaction will not be familiar with these requirements and may inadvertently create compliance issues that delay or complicate completion. A specialist broker has navigated these requirements many times and manages them as a routine part of the process.

The cost of a slow sale

A slow sale is not just an inconvenience – it has a direct financial cost. During an extended sale process, the seller is typically managing the sale alongside running their practice, which takes significant management time and energy away from the business itself. Revenue may plateau or decline as the owner’s attention is divided. Staff uncertainty may increase staff turnover, which reduces the value of the practice the buyer is acquiring. And market conditions can change: the multiple that was achievable at instruction may be lower twelve months later if the market has softened or if specific buyers who were interested have made acquisitions elsewhere.

When timing matters most

The optimal time to sell is when the practice is growing, your recurring revenue is strong, and you have at least two years of solid financial performance to show a buyer. Waiting until the practice is declining, or until personal circumstances force a rushed sale, almost always results in a lower multiple and worse terms. A specialist broker can advise on whether your practice is ready to maximise value or whether a period of positioning would significantly improve your outcome.

6. Negotiation – The Difference Between a Good Deal and the Best Deal

Most accountancy practice owners have never sold a business before and will only do so once. The buyer, whether an individual expanding their practice or a PE-backed consolidator, may have completed dozens of acquisitions. This experience asymmetry puts the unrepresented seller at a significant disadvantage in negotiations, not necessarily because the buyer is acting in bad faith, but simply because the buyer understands the process, the market, and the leverage points far better than a first-time seller.

A specialist broker levels this asymmetry. They have negotiated many similar transactions, understand the typical range of outcomes on every variable from headline price to earn-out conditions to transition support obligations, and know when a buyer’s position is genuinely fixed and when it is an opening negotiation tactic. They also provide the seller with the psychological distance to negotiate effectively – it is far easier for a broker to push back firmly on an unreasonable term than it is for a seller who has built the practice over twenty years and has an emotional investment in completing the sale.

Managing multiple offers and competitive tension

One of the most powerful tools in any negotiation is competitive tension – the genuine presence of more than one interested party. Specialist brokers structure the marketing process specifically to generate multiple offers simultaneously, creating a competitive environment in which buyers understand that they need to put their best terms forward rather than testing how low the seller will go. This alone can add a meaningful premium to the final price and, equally importantly, can improve non-price terms such as payment structure, earn-out conditions, and transition support obligations.

A seller managing their own sale typically approaches buyers sequentially – speaking with one, allowing weeks to pass, then approaching another. This sequential process eliminates competitive tension and gives each buyer the luxury of time and minimal pressure to improve their offer. A specialist broker generates simultaneous interest and manages the timeline so that multiple buyers are making decisions at the same point, creating the conditions for the best possible outcome.

7. Transition Planning – Protecting Value After the Deal Is Done

The period immediately after a practice sale is arguably as important as the sale process itself. Client retention during the transition – the weeks and months during which clients are introduced to the new owner, begin working with new staff, and adjust to potentially different ways of working – is the primary determinant of whether the seller receives their full earn-out and whether the buyer considers the acquisition a success.

A specialist broker advises on transition planning as an integral part of the sale process, not as an afterthought. This begins with the structure of the transition period itself: how long will the selling partner remain involved, in what capacity, at what compensation, and with what authority? A transition that is too short may result in clients leaving before relationships with the new team are established. A transition that is too long, or in which the selling partner retains too much authority, may prevent the buyer from making necessary changes and delay the integration of the practice into the acquiring firm.

Client communication – the make or break moment

The formal communication to clients that the practice is under new ownership is the single most important event in the transition period. How it is managed, what it says, and how it is timed directly affects client retention. A poorly worded or poorly timed communication – or worse, a situation where clients find out informally before the official announcement – can trigger a wave of practice changes that damages both the seller’s earn-out and the buyer’s return on investment.

Specialist brokers have experience of dozens of these communications and can advise on the precise wording, format, timing, and follow-up strategy that maximises client retention. They know which clients are likely to be most sensitive, how to position the change as positive rather than disruptive, and how to ensure that the new owner is introduced in a way that builds immediate confidence. This advice is not theoretical – it is grounded in what has and has not worked in actual transactions in the accountancy sector.

8. Common Mistakes When Selling Without a Specialist Broker

The pattern of mistakes made by accountancy practice owners who sell without specialist broker support is remarkably consistent. Understanding these mistakes is the most direct way to understand the value a specialist broker provides.

Undervaluing the practice at the outset. Sellers who have not benchmarked against current market multiples frequently price their practice below market value, leaving significant money on the table. Once a price has been advertised, it is very difficult to increase it without losing credibility with buyers who have already seen the listing.

Revealing identity too early and too broadly. Unmanaged marketing on general business sale platforms frequently exposes the identity of the practice before a non-disclosure agreement is in place. The consequences – staff anxiety, client uncertainty, referral partner concern – reduce the value of the practice before a buyer is even found.

Accepting the first credible offer. A seller managing their own process who receives a credible offer after months of unproductive searching is strongly tempted to accept it immediately, even if the terms are not optimal. A specialist broker managing a competitive process is never in this position, because multiple qualified offers are typically generated simultaneously.

Failing to understand earn-out risks. Earn-out provisions that seem straightforward on first reading frequently contain conditions that are very difficult to satisfy in practice. Sellers without specialist advice often sign earn-out agreements they do not fully understand, and are then surprised when the deferred consideration is not paid in full.

Neglecting the tax structure of the sale. The difference between income tax treatment and capital gains tax treatment on elements of the consideration can be very significant. Business Asset Disposal Relief on qualifying capital gains currently allows a 10 percent rate on up to £1 million of lifetime gains, compared with income tax rates of up to 45 percent. The opportunity to structure the deal to maximise this relief requires specialist tax advice, which a broker will coordinate alongside the transaction.

Underestimating the management time required. A self-managed practice sale requires the owner to handle enquiries, due diligence requests, legal negotiations, and regulatory requirements simultaneously with running the practice. This is a significant management burden that typically results in either the sale taking far longer than expected or the practice’s performance declining during the sale period.